PAY NOW, OR PAY LATER?

Have you ever gotten a call from one of these microfinance banks to take a loan? Or maybe you got an SMS to bail out a friend or relative who is unable to pay back a loan. Well, buckle up your seatbelt and make sure your phone is at hand to receive more messages because Buy Now, Pay Later (BNPL) is taking roots in Nigeria.

Of the several problems FinTechs try to solve in the industry, two stand out — payment and funding, because of the impact they make. From a macroeconomic standpoint, funding is very important because it drives consumption — the most important element of the GDP equation. Consumers pump demand, which pumps production, which pumps national income. When banks provide funding to corporations and they produce goods and services that nobody consumes it’s bad news, both for the company and the bank. However, when banks give out loans to consumers they are able to purchase goods and services they ordinarily can’t afford and corporations benefit because they can produce more. This is why governments give grants and offer special vehicle loans to certain sectors of an economy. It is for the same reason the Nigerian apex bank insists on the 65% bank loan to deposit ratio. However, banks, in a bid to limit their credit risk, continue to offer facilities to corporates and high net worth individuals.

Non-bank financial institutions like Carbon, CDCare, PayQart, O3 and Credpal, to mention a few, are changing the lending landscape with BNPL. You can now buy a phone, a car, a shoe, a blender, a book, and spread the payment. You can shop online on just about any ecommerce site and have the option to pay now, or pay later. The early adopters in Nigeria include Zoomba.ng, Shopsfit.com, Ebeosi.com, Slickmobile.com, Justfones.ng, spredda.com. In fact, the options are so flexible that you can choose how many months you want to pay and which lender you want to use. If you wish, you can opt for a layaway method where you pay in installments without taking a loan but the store keeps the goods and only delivers after full payment is made. The interesting thing is, most of these lenders charge zero interest! It got interesting for me when I started noticing how Autocheck dotted Lagos streets with their signposts. So BNPL is not only online. A good percentage of car dealers are getting into partnership with Autocheck to sell cars to clients who want to buy now and spread the payment. Several real estate agents are selling homes and plots of lands by installments. Add to the list Telcos that lend airtime and debit later. Recently, Max and Bolt got into a deal to provide riders with bikes on hire purchase. It seems the American credit lifestyle is finally coming home.

What does this all mean for individuals, banks and the nation? First of all, everyone needs to watch their credit rating. Your rating is now more important than your necessary food. Banks and FinTechs are mining credit data from a centralized credit bureau and can easily woo any customer or disenfranchise anyone from the system with another centralized interbank system using BVN. Secondly, securitization will only be required for big ticket loans. The days of 100% cash collateral to get a credit card reserved for only 20% of banks’ customers will soon be behind us. Credpal and O3 are giving out credit cards to everyone and anyone. Financial institutions have begun to understand that data and customer profiling is more important than security in the retail space. Finally, if the BNPL trend holds up, and by that I mean if default rate is negligible (Ok, I agree, that’s not possible), I see a boom business cycle ahead. According to Research and Market, there is a 26% compound annual growth projection from $204m in 2021 to $1.7b in 2028 for BNPL.

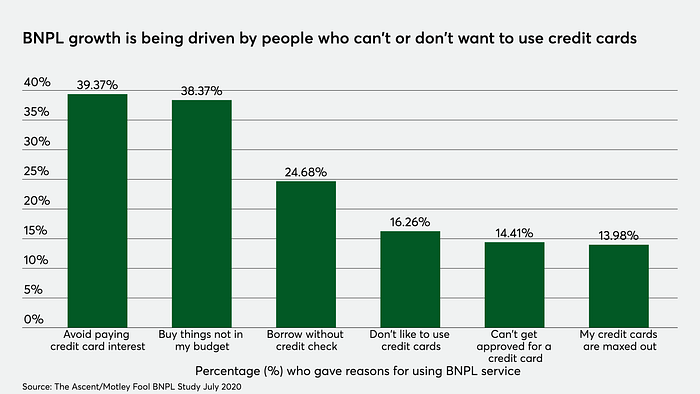

Nevertheless, with every boom comes a burst. The 2008 global financial meltdown is still fresh in our memories and is no different from today’s trend. The gen-Z consumers love to spend before they earn and are extremely social. BNPL is not only trending locally, it is a global phenomenon across all the continents. Top ten worldwide BNPL include: Klarna, Affirm, Quadpay, PayIn4 (PayPal), Afterpay, M-Kopa, Payflex, ZIP and OpenPay. The challenge with paying later is that tomorrow is always shorter than today unless you earn more than you spend. The burden of repayment is real and if you’re not disciplined, your upkeep becomes your downfall when your outflow exceeds your inflow.

On the potential side of things, there are several points to exploit, one of which is that currently, majorly salary earners benefit from BNPL. Self-employed and employees of SMEs are deprived of the privilege of participating in the system yet most of the people in this category are the actual targets of financial inclusion. They are the petty traders, vulcanizers, hairdressers, mechanics, subsistence farmers etc. These guys belong to cooperatives where they get loans, and understand credit rating more than the average banked folks. Unfortunately, there is limited data to support their discipline. Coincidentally, they are the ‘spend all you earn’ category in society. If there is a way to pull them in (maybe a startup can digitize their thrift & credit history with cooperatives), business owners represent over 45 million individuals of the 106 million productive Nigerian adults as compared to only 8 million in the formal sector, according to EfInA.

Another area of potential is the stock market. BNPL investment in the capital market will ensure liquidity in both the secondary and primary market. Investors know that leverage is a game changer when you trade stocks. Brokers need funding to support big ticket trades, as well as implement derivative trading and Contracts For Difference (cfd). With a cfd, a trader can enter into a big trade with a small amount of money. The difference between the value of the trade and what the trader has at hand is provided by his broker. If the trade goes his way, the broker subtracts the loan value and the trader keeps all the profit. Thus, with cfds, traders are able to double their investment in a day’s trade. However, if the trade goes against the trader, the broker secures his capital and the trader’s loss is limited to his small investment. For fourteen days, MTN shares will be on offer to the public. These are not new allotments, they are Offer For Sale, and they are already discounted; plus the company just got approval in principle to launch a payment service bank, the share price can only go north. However, with no funds, the opportunity slips — enter BNPL (Act 1, Scene 1).

A lot has changed since microfinance banks flooded the market with loans. In the area of rent, they are helping tenants pay rent on a monthly basis rather than on an annual basis, albeit at cut-throat rate. A typical BNPL solution would have been to offer the landlord the option of securing the rent upfront at a cost and spreading the payment for the tenant at no interest. That’s the paradigm shift that provides the value proposition for BNPL. A similar use case is school fees payment. Of course, it will take some time with a little bit of help for this change to be completely accepted by society. For the kind of liquidity required in this burgeoning industry, it would be good to have a weekly salary system rather than a monthly pay. It would also help if regulators come together (Central bank, Consumer protection, Data protection) and issue a guideline/act on fair debt collection. Thankfully, NITDA and FCCPC have started raising their eyebrows.

Finally, if financial inclusion is a worthy goal of the government, and if all this talk makes sense, then PSBs should be granted lending rights because they can play in this field.